时间序列最简单的预测方法

均值法

\[\hat{y}_{T+h | T}=\left(y_{1}+\cdots+y_{T}\right) / T\]

一个例子

library(tidyverse)## -- Attaching packages ---------------------------------------------------- tidyverse 1.3.0 --## √ ggplot2 3.3.0 √ purrr 0.3.3

## √ tibble 2.1.3 √ dplyr 0.8.5

## √ tidyr 1.0.2 √ stringr 1.4.0

## √ readr 1.3.1 √ forcats 0.5.0## -- Conflicts ------------------------------------------------------- tidyverse_conflicts() --

## x dplyr::filter() masks stats::filter()

## x dplyr::lag() masks stats::lag()library(forecast)## Registered S3 method overwritten by 'quantmod':

## method from

## as.zoo.data.frame zoolibrary(fpp2)## 载入需要的程辑包:fma## 载入需要的程辑包:expsmoothlibrary(ggfortify)## Registered S3 methods overwritten by 'ggfortify':

## method from

## autoplot.Arima forecast

## autoplot.acf forecast

## autoplot.ar forecast

## autoplot.bats forecast

## autoplot.decomposed.ts forecast

## autoplot.ets forecast

## autoplot.forecast forecast

## autoplot.stl forecast

## autoplot.ts forecast

## fitted.ar forecast

## fortify.ts forecast

## residuals.ar forecastlibrary(ggthemes)

library(timetk)

library(DT)

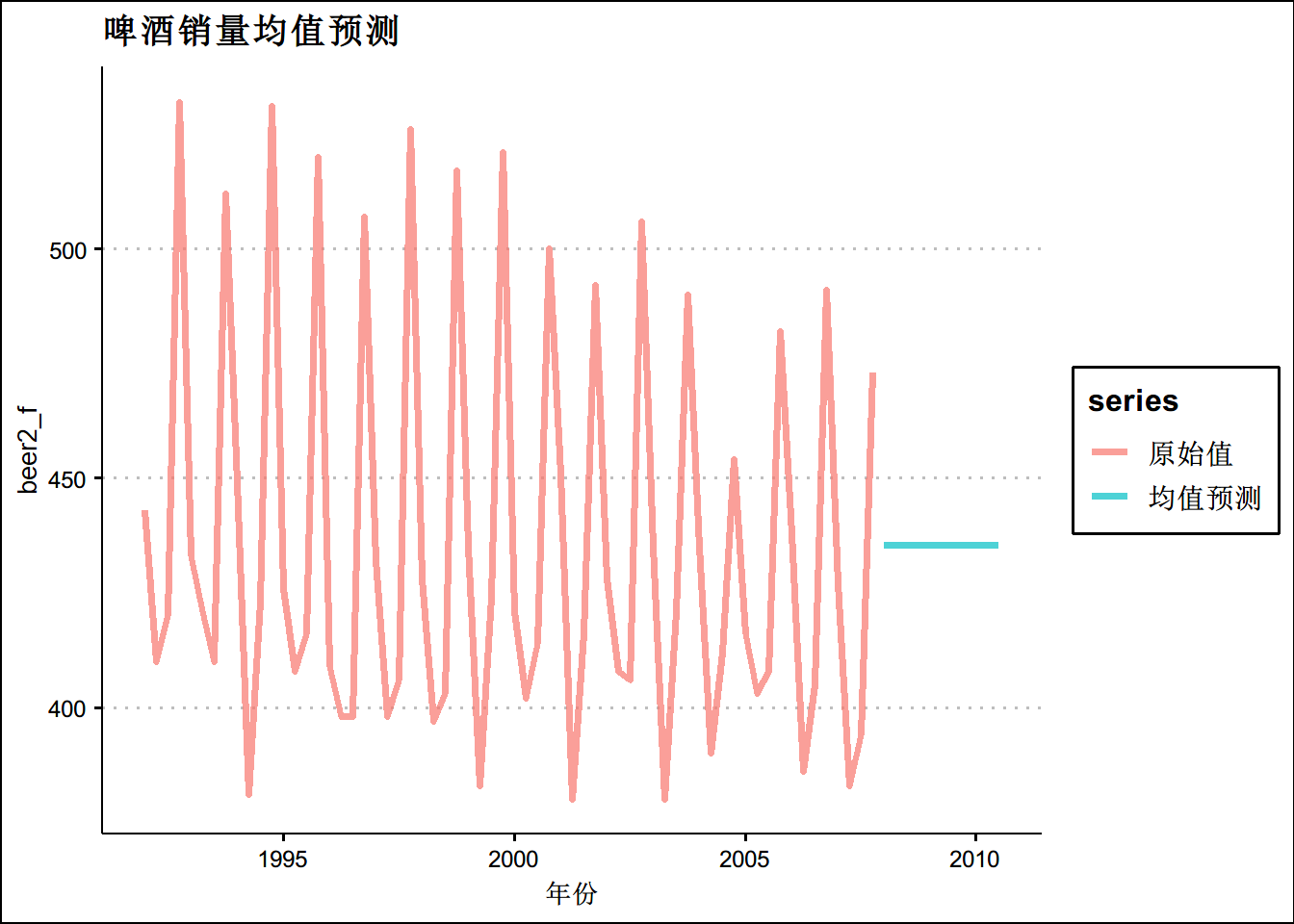

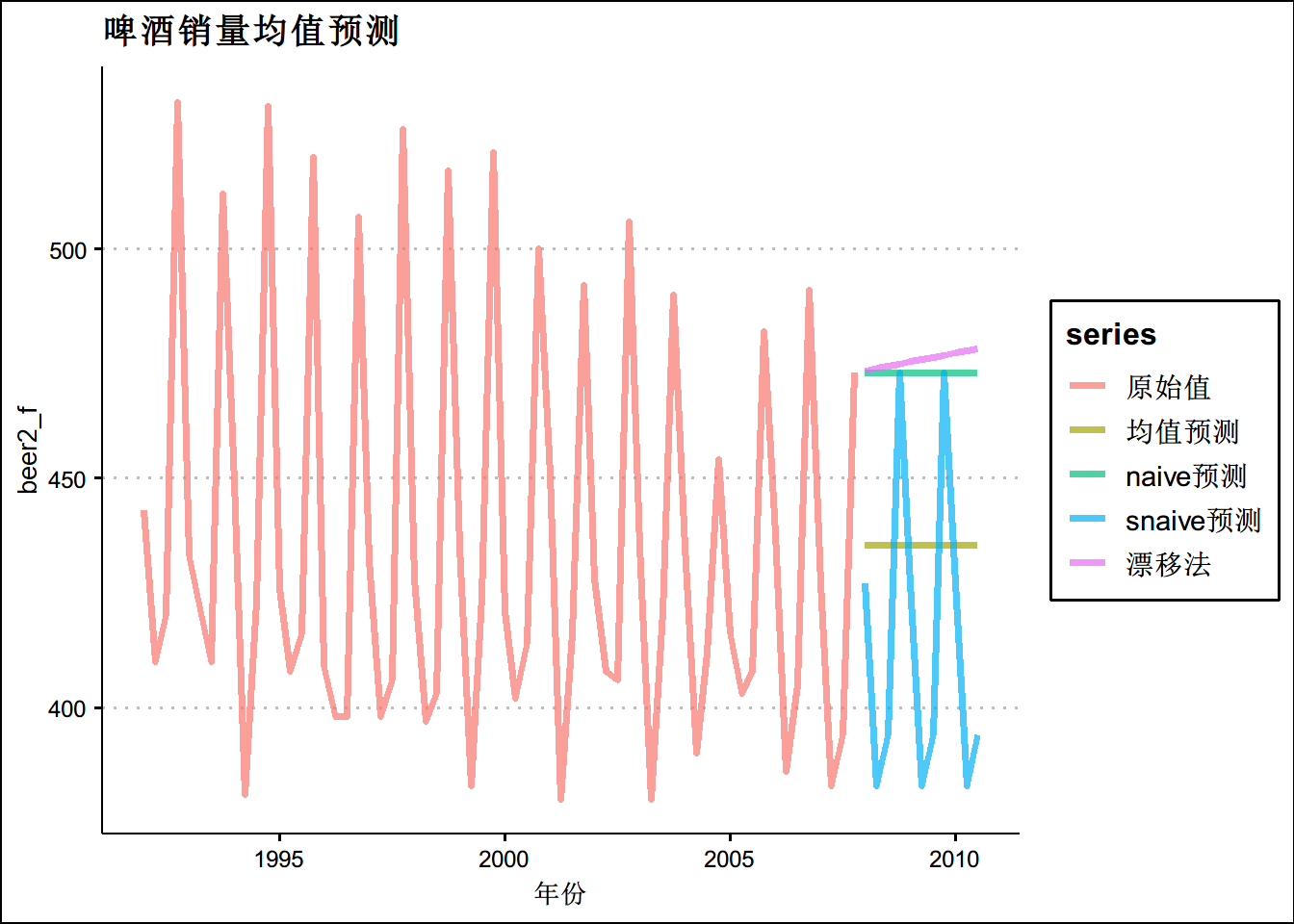

# 设定数据

beer2 <- window(ausbeer,start=1992,end=c(2007,4))

# 均值预测

k<-meanf(beer2,h=11)

k$mean## Qtr1 Qtr2 Qtr3 Qtr4

## 2008 435.375 435.375 435.375 435.375

## 2009 435.375 435.375 435.375 435.375

## 2010 435.375 435.375 435.375beer2_f <- ts.union(beer2,k$mean)

colnames(beer2_f) <- c("原始值",'均值预测')

autoplot(beer2_f,size=1.4,alpha=0.7)+theme_clean()+ggtitle("啤酒销量均值预测")+

xlab("年份")

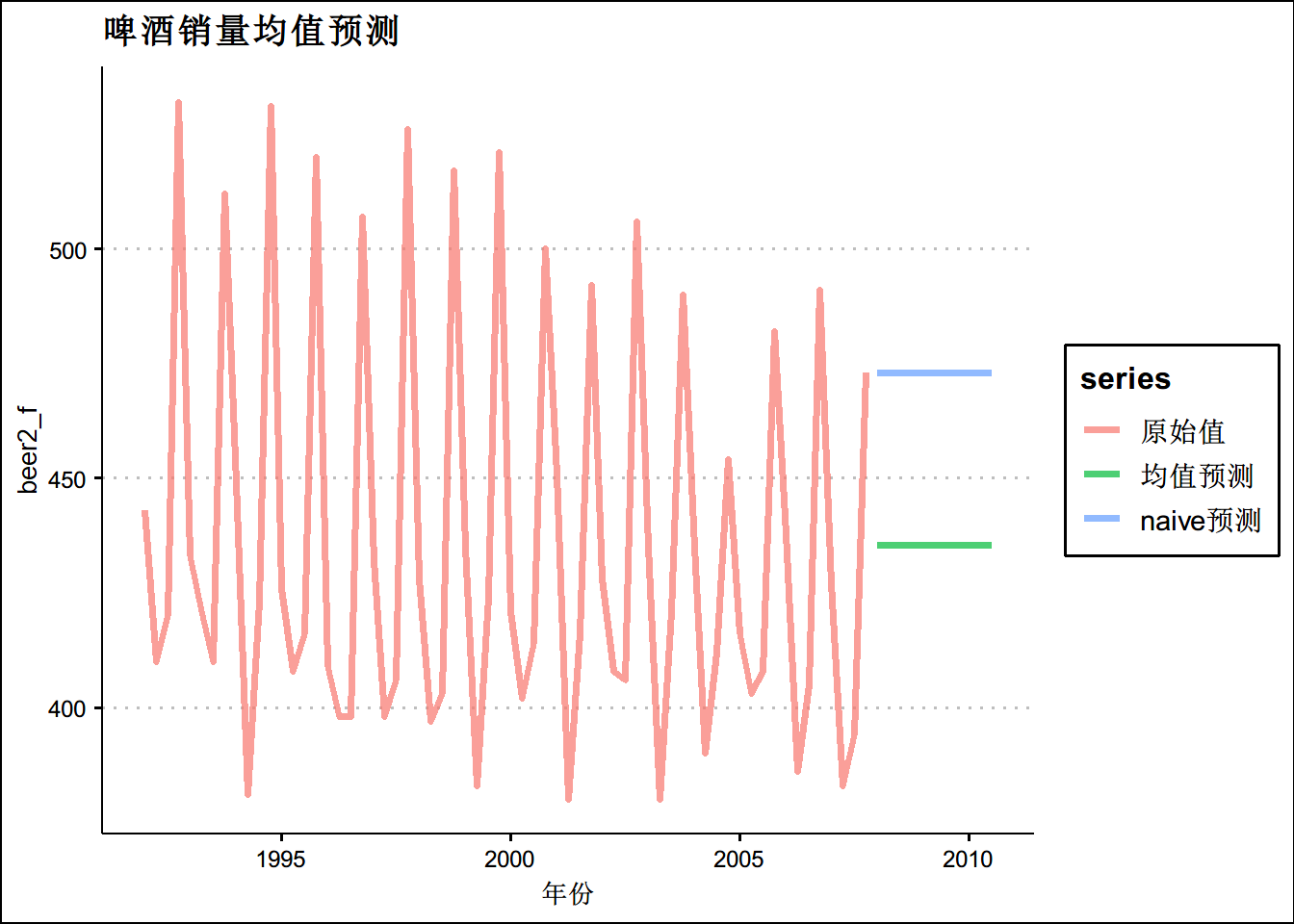

#naive预测

n <- naive(beer2,h=11)

n$mean## Qtr1 Qtr2 Qtr3 Qtr4

## 2008 473 473 473 473

## 2009 473 473 473 473

## 2010 473 473 473beer2_f <- ts.union(beer2,k$mean,n$mean)

colnames(beer2_f) <- c("原始值",'均值预测','naive预测')

autoplot(beer2_f,size=1.4,alpha=0.7)+theme_clean()+ggtitle("啤酒销量均值预测")+

xlab("年份")

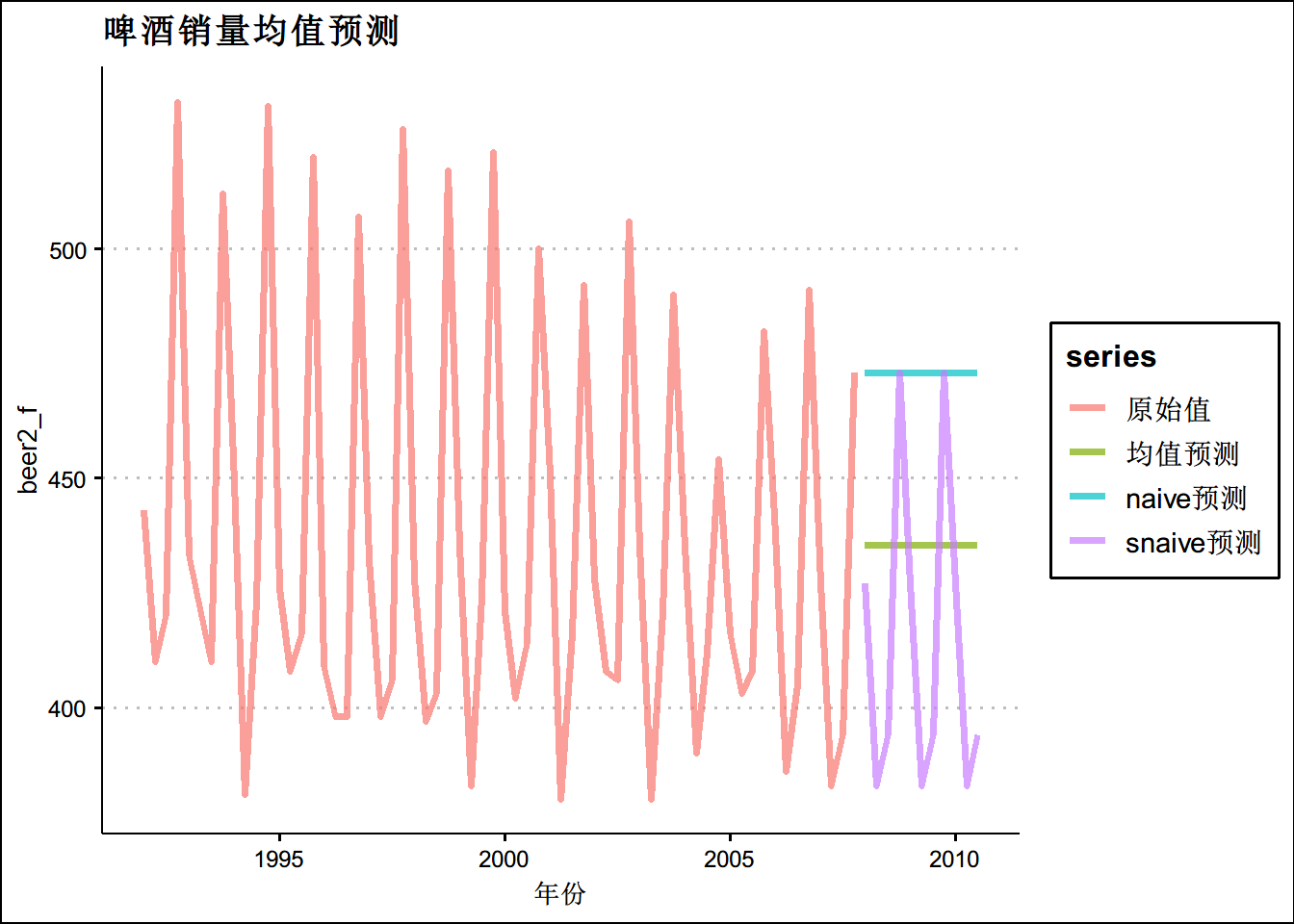

#snaive预测

s_n <- snaive(beer2,h=11)

s_n$mean## Qtr1 Qtr2 Qtr3 Qtr4

## 2008 427 383 394 473

## 2009 427 383 394 473

## 2010 427 383 394beer2_f <- ts.union(beer2,k$mean,n$mean,s_n$mean)

colnames(beer2_f) <- c("原始值",'均值预测','naive预测','snaive预测')

autoplot(beer2_f,size=1.4,alpha=0.7)+theme_clean()+ggtitle("啤酒销量均值预测")+

xlab("年份")

#漂移法

d<- rwf(beer2,h=11,drift = T)

d$mean## Qtr1 Qtr2 Qtr3 Qtr4

## 2008 473.4762 473.9524 474.4286 474.9048

## 2009 475.3810 475.8571 476.3333 476.8095

## 2010 477.2857 477.7619 478.2381beer2_f <- ts.union(beer2,k$mean,n$mean,s_n$mean,d$mean)

colnames(beer2_f) <- c("原始值",'均值预测','naive预测','snaive预测','漂移法')

autoplot(beer2_f,size=1.4,alpha=0.7)+theme_clean()+ggtitle("啤酒销量均值预测")+

xlab("年份")

预测精度的例子

beer2 <- window(ausbeer,start=1992,end=c(2007,4))

beerfit1 <- meanf(beer2,h=10)

beerfit2 <- rwf(beer2,h=10)

beerfit3 <- snaive(beer2,h=10)

beer3 <- window(ausbeer, start=2008)

accuracy(beerfit1, beer3)## ME RMSE MAE MPE MAPE MASE ACF1

## Training set 0.000 43.62858 35.23438 -0.9365102 7.886776 2.463942 -0.10915105

## Test set -13.775 38.44724 34.82500 -3.9698659 8.283390 2.435315 -0.06905715

## Theil's U

## Training set NA

## Test set 0.801254accuracy(beerfit2, beer3)## ME RMSE MAE MPE MAPE MASE

## Training set 0.4761905 65.31511 54.73016 -0.9162496 12.16415 3.827284

## Test set -51.4000000 62.69290 57.40000 -12.9549160 14.18442 4.013986

## ACF1 Theil's U

## Training set -0.24098292 NA

## Test set -0.06905715 1.254009accuracy(beerfit3, beer3)## ME RMSE MAE MPE MAPE MASE ACF1

## Training set -2.133333 16.78193 14.3 -0.5537713 3.313685 1.0000000 -0.2876333

## Test set 5.200000 14.31084 13.4 1.1475536 3.168503 0.9370629 0.1318407

## Theil's U

## Training set NA

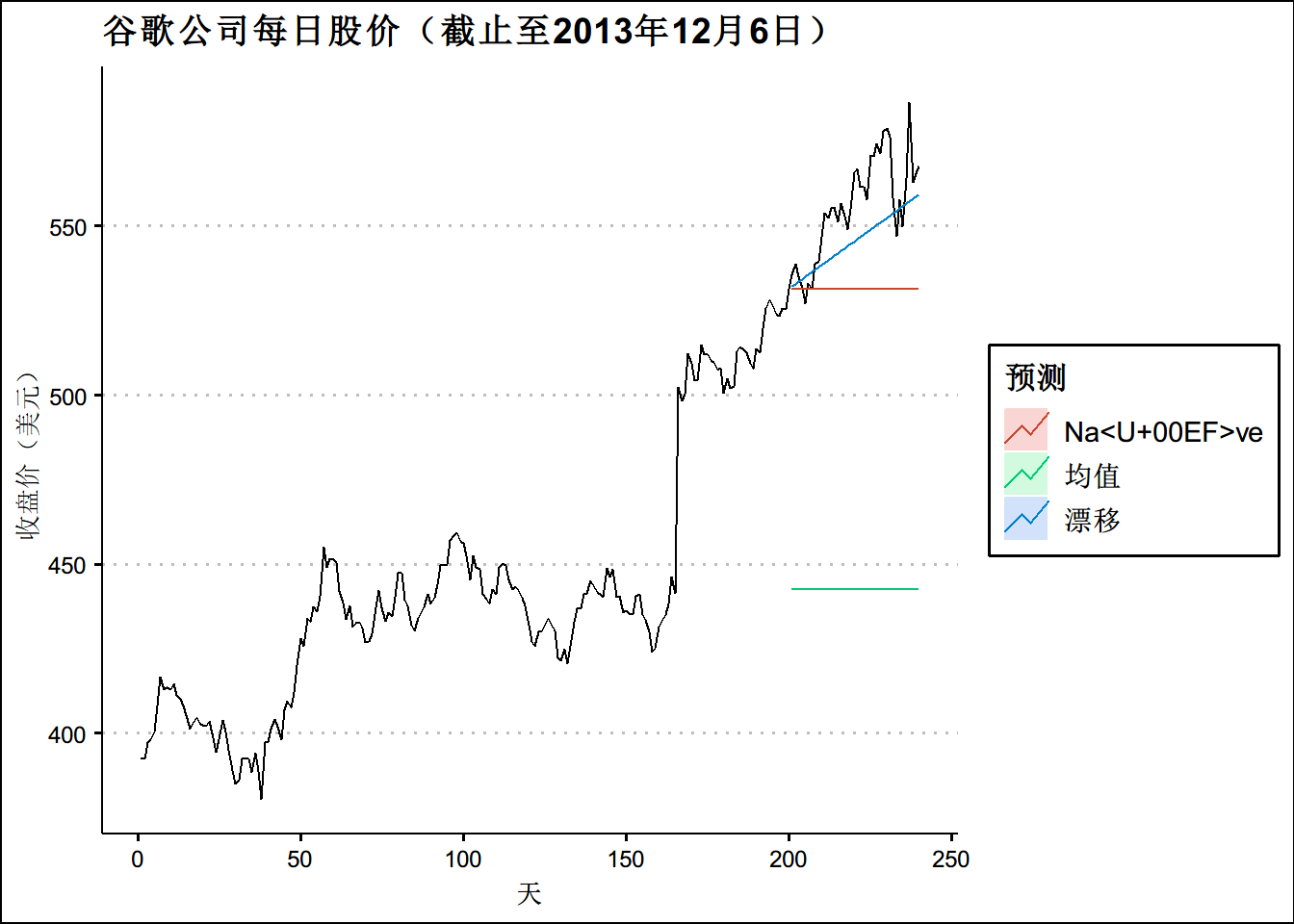

## Test set 0.298728#这里我们直接使用autoplayer包

googfc1 <- meanf(goog200, h=40)

googfc2 <- rwf(goog200, h=40)

googfc3 <- rwf(goog200, drift=TRUE, h=40)

autoplot(subset(goog, end = 240)) +

autolayer(googfc1, PI=FALSE, series="均值") +

autolayer(googfc2, PI=F, series="Naïve") +

autolayer(googfc3, PI=FALSE, series="漂移") +

xlab("天") + ylab("收盘价(美元)") +

ggtitle("谷歌公司每日股价(截止至2013年12月6日)") +

guides(colour=guide_legend(title="预测"))+

theme(text = element_text(family = "STHeiti"))+

theme(plot.title = element_text(hjust = 0.5)) +

theme_clean()

#计算预测精度

googtest <- window(goog, start=201, end=240)

accuracy(googfc1, googtest)## ME RMSE MAE MPE MAPE MASE

## Training set -4.296286e-15 36.91961 26.86941 -0.6596884 5.95376 7.182995

## Test set 1.132697e+02 114.21375 113.26971 20.3222979 20.32230 30.280376

## ACF1 Theil's U

## Training set 0.9668981 NA

## Test set 0.8104340 13.92142accuracy(googfc2, googtest)## ME RMSE MAE MPE MAPE MASE

## Training set 0.6967249 6.208148 3.740697 0.1426616 0.8437137 1.000000

## Test set 24.3677328 28.434837 24.593517 4.3171356 4.3599811 6.574582

## ACF1 Theil's U

## Training set -0.06038617 NA

## Test set 0.81043397 3.451903accuracy(googfc3, googtest)## ME RMSE MAE MPE MAPE MASE

## Training set -5.998536e-15 6.168928 3.824406 -0.01570676 0.8630093 1.022378

## Test set 1.008487e+01 14.077291 11.667241 1.77566103 2.0700918 3.119002

## ACF1 Theil's U

## Training set -0.06038617 NA

## Test set 0.64732736 1.709275移动平均,简单移动平均的阶数常常是奇数阶,在阶数为m=2k+1的移动平均中,中心值两侧各有k个观测值可以被平均

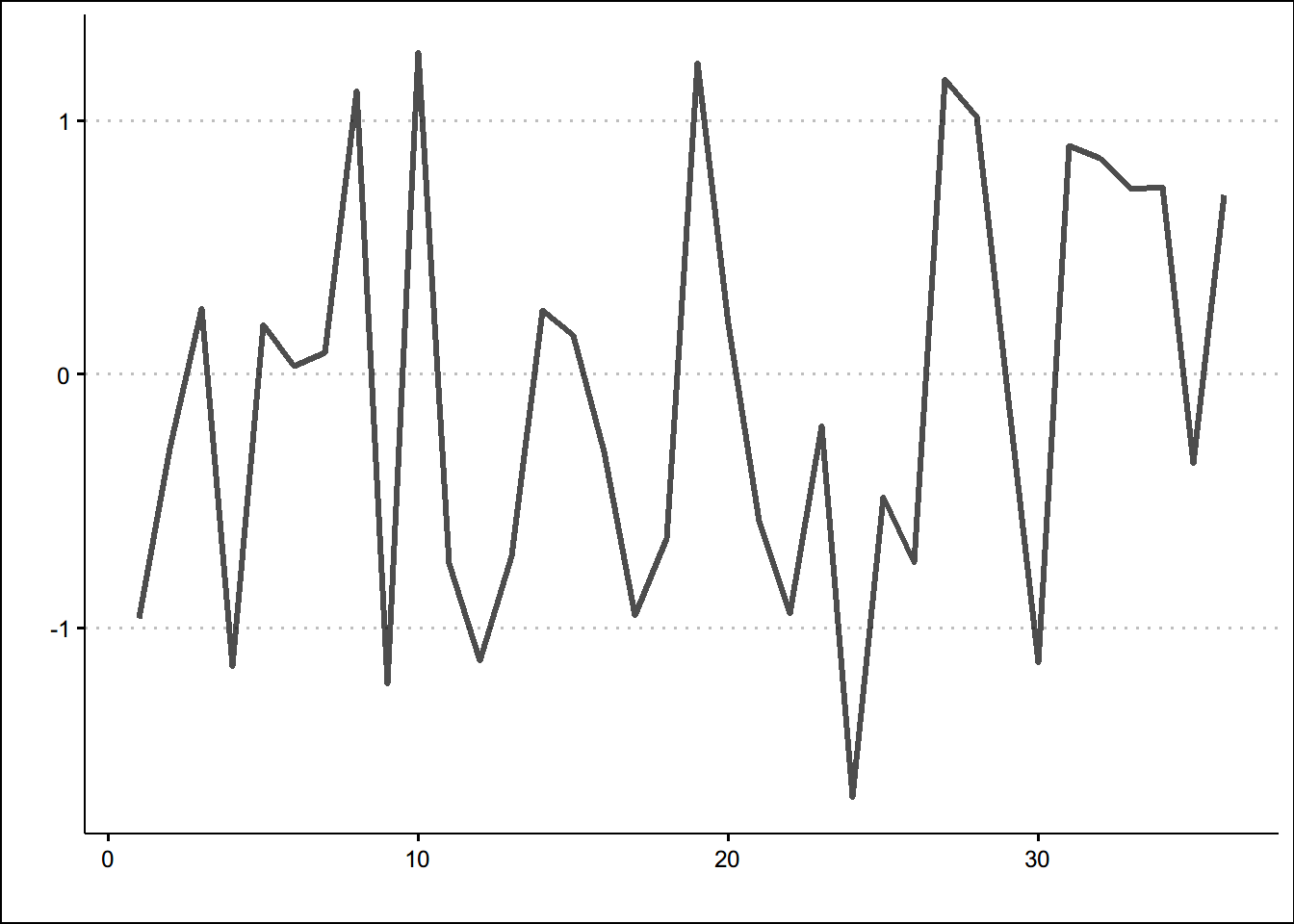

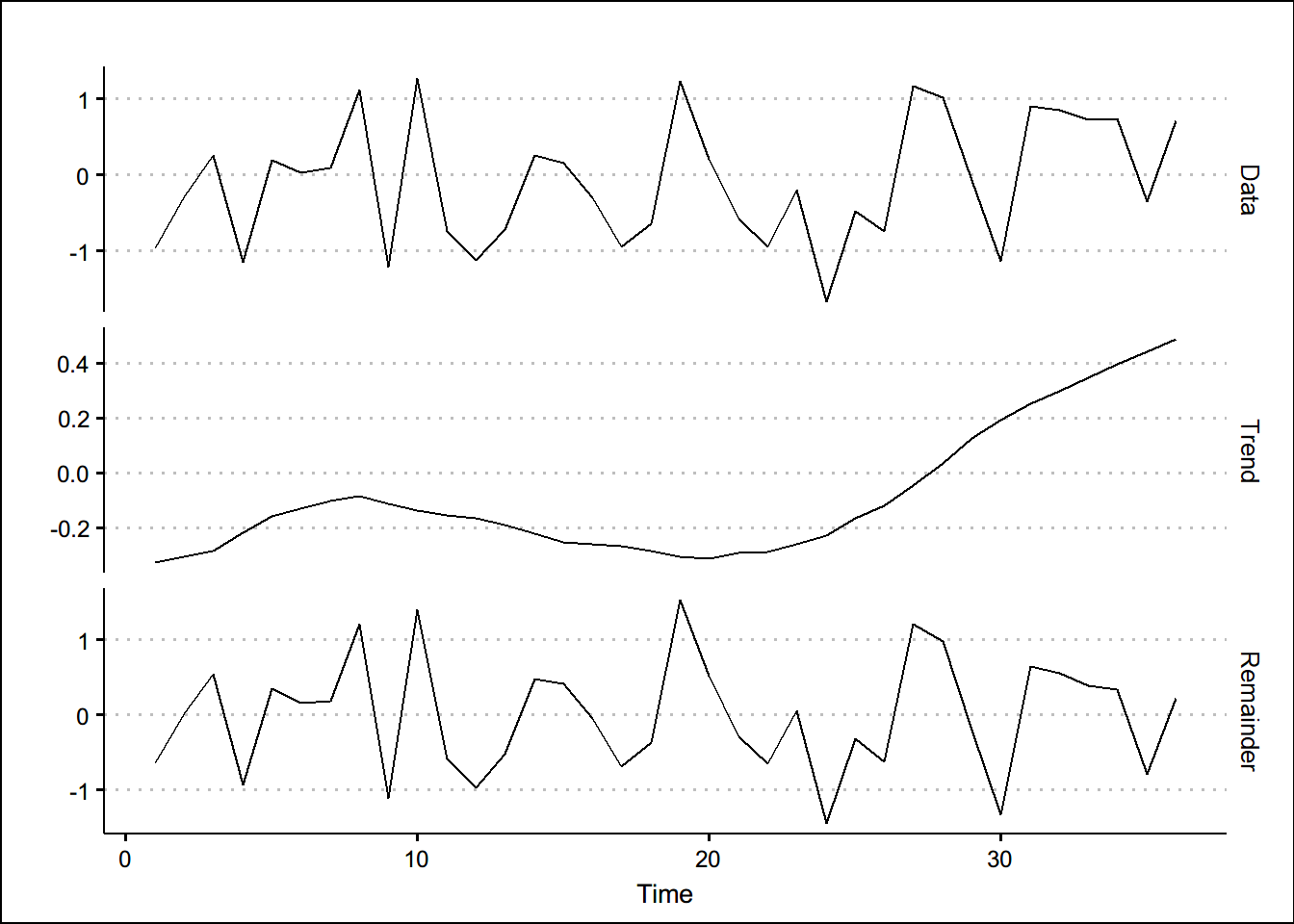

先看一个白噪声的例子

set.seed(3)

wn <- ts(rnorm(36))

autoplot(wn,size =1.1,alpha = 0.7)+theme_clean()

autoplot(mstl(wn))+theme_clean()

data(elecsales)

ele <- timetk::tk_tbl(elecsales)

ele <- ele %>%

mutate(mm = ma(elecsales,order = 5))

ele %>% datatable(colnames = c("年份","原始数据","MA5"))#ma5第一个数是2381.53,具体计算方式如下:

paste("这个数是这样得到的:",mean(pull(ele[1:5,'value'])),"下面会显示一个TRUE")## [1] "这个数是这样得到的: 2381.53 下面会显示一个TRUE"ele[3,3]==mean(pull(ele[1:5,'value']))## mm

## [1,] TRUE#ma5图

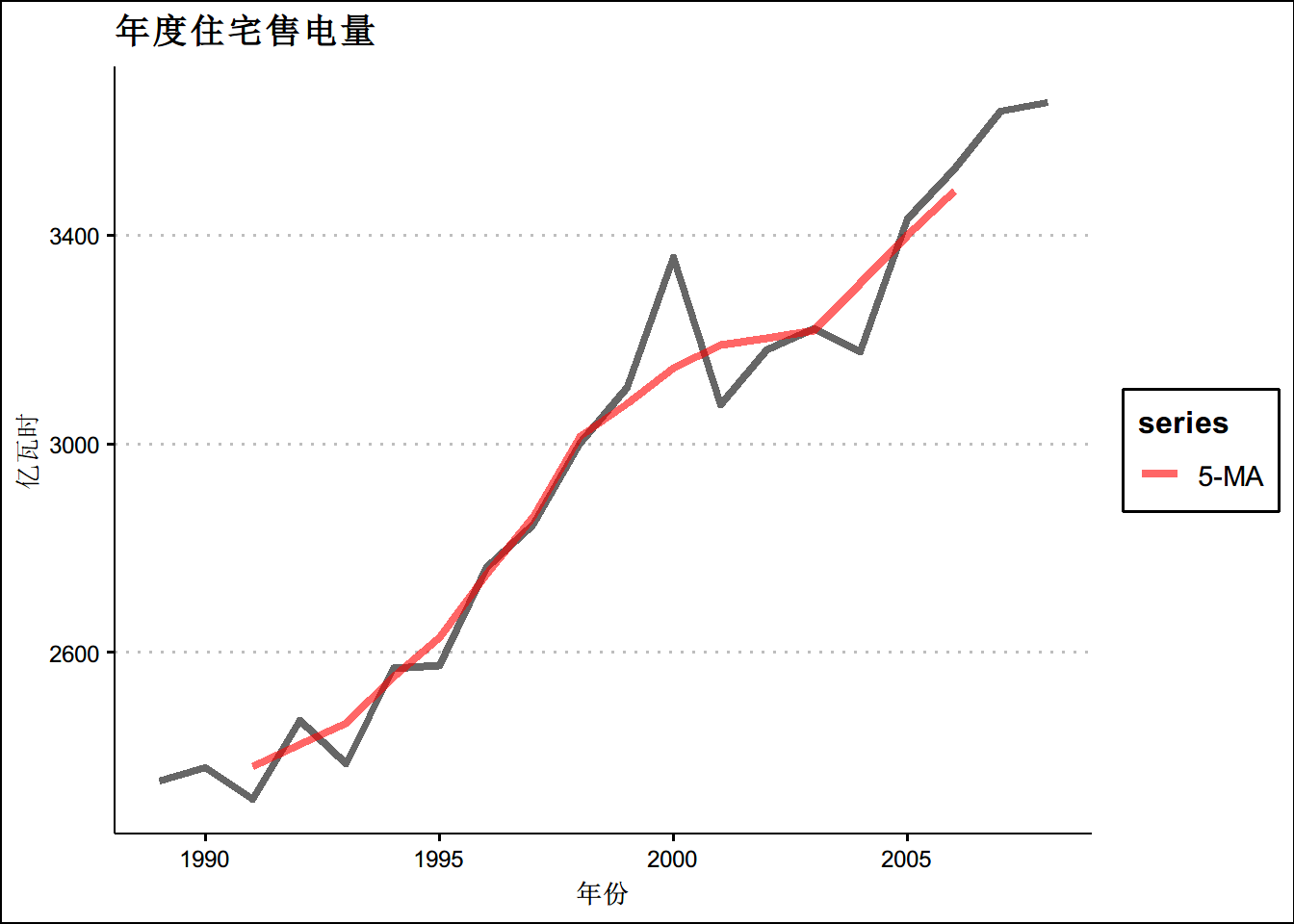

autoplot(elecsales,size=1.5,alpha=0.6 ,series="原始数据") +

autolayer(ma(elecsales,5), series="5-MA",size=1.5,alpha=0.6) +

xlab("年份") + ylab("亿瓦时") +

ggtitle("年度住宅售电量") +

scale_colour_manual(values=c("Data"="grey50","5-MA"="red"),

breaks=c("Data","5-MA"))+

theme(text = element_text(family = "STHeiti"))+

theme(plot.title = element_text(hjust = 0.5))+theme_clean()

#ma3图

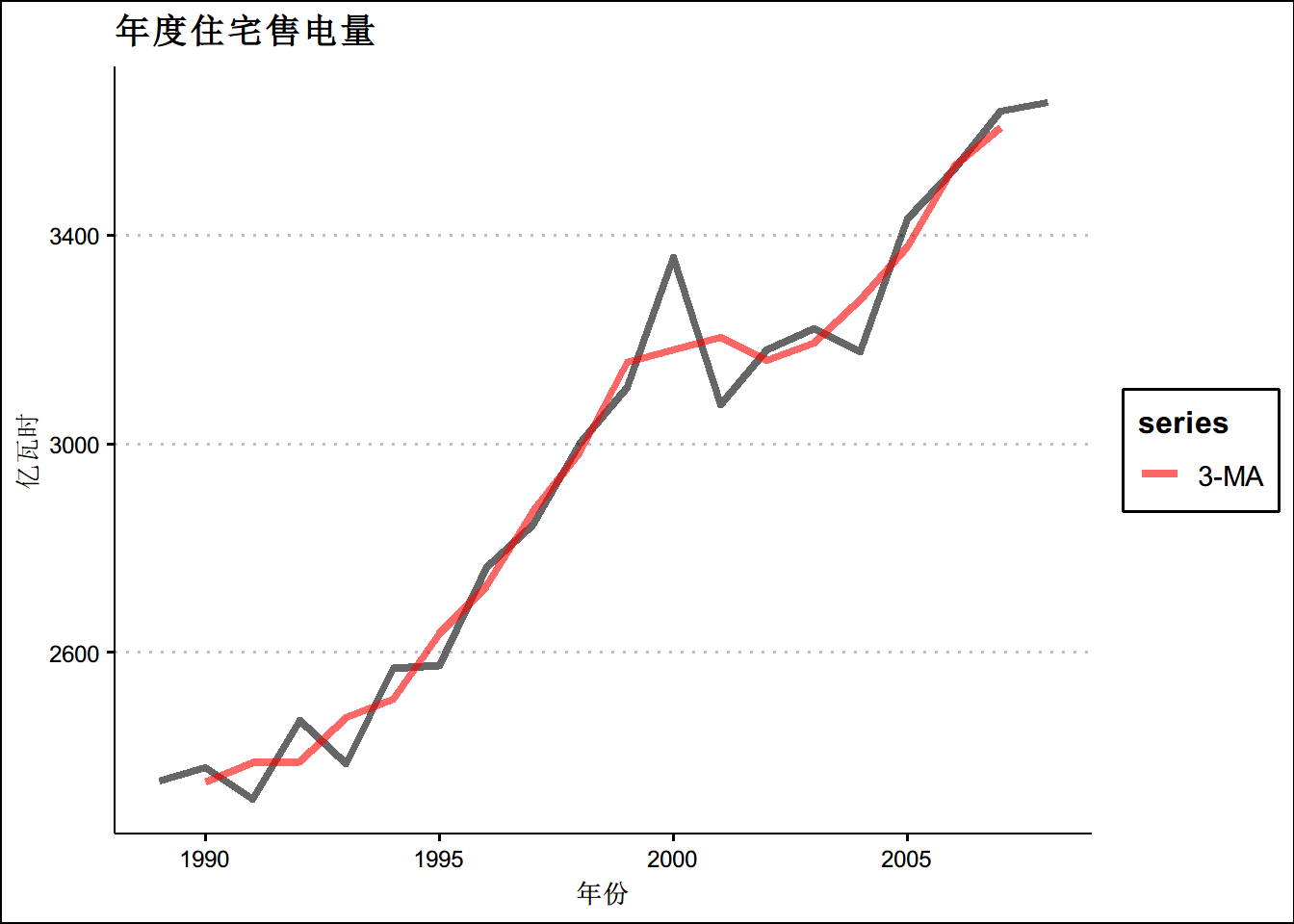

autoplot(elecsales,size=1.5,alpha=0.6 ,series="原始数据") +

autolayer(ma(elecsales,3), series="3-MA",size=1.5,alpha=0.6) +

xlab("年份") + ylab("亿瓦时") +

ggtitle("年度住宅售电量") +

scale_colour_manual(values=c("Data"="grey50","3-MA"="red"),

breaks=c("Data","3-MA"))+

theme(text = element_text(family = "STHeiti"))+

theme(plot.title = element_text(hjust = 0.5))+theme_clean()

#ma3图

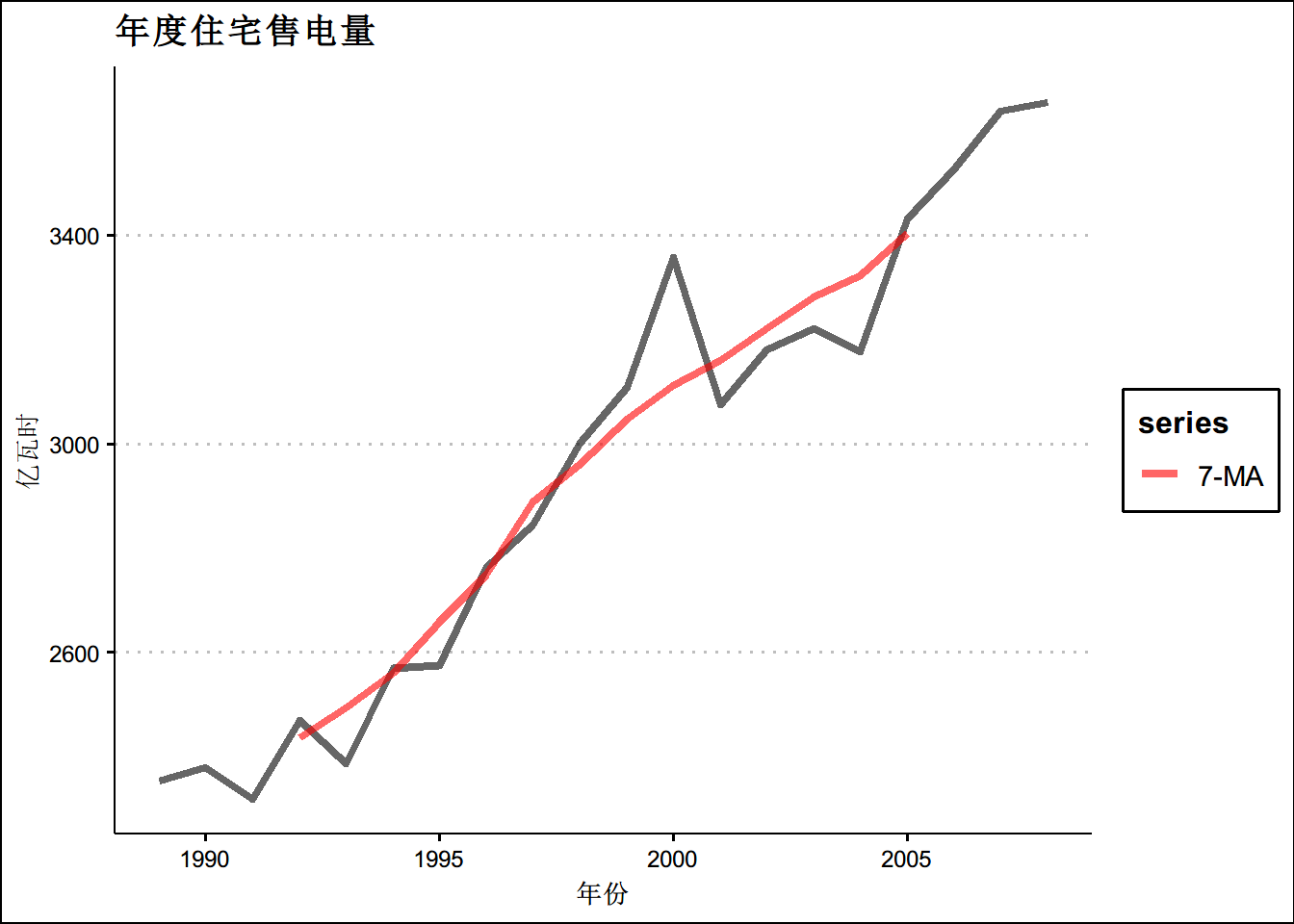

autoplot(elecsales,size=1.5,alpha=0.6 ,series="原始数据") +

autolayer(ma(elecsales,7), series="7-MA",size=1.5,alpha=0.6) +

xlab("年份") + ylab("亿瓦时") +

ggtitle("年度住宅售电量") +

scale_colour_manual(values=c("Data"="grey50","7-MA"="red"),

breaks=c("Data","7-MA"))+

theme(text = element_text(family = "STHeiti"))+

theme(plot.title = element_text(hjust = 0.5))+theme_clean() ## 移动平均的移动平均

## 移动平均的移动平均

beer2 <- window(ausbeer,start=1992)

beer2_df <- timetk::tk_tbl(beer2)

beer2_df <- beer2_df %>%

mutate(mm = ma(beer2,order = 4,centre = F)) %>%

mutate(mmm = ma(beer2,order = 4,centre = T))

beer2_df %>% datatable(colnames = c("年份","原始数据","MA4","2*4MA"))# 450 = (451.25+448.75)/2使用线性模型对时间序列进行预测

\[y_{t}=\beta_{0}+\beta_{1} t+\beta_{2} d_{2, t}+\beta_{3} d_{3, t}+\beta_{4} d_{4, t}+\varepsilon_{t}\]

beer2 <- window(ausbeer, start=1992)

fit.beer <- tslm(beer2 ~ trend + season)

summary(fit.beer)##

## Call:

## tslm(formula = beer2 ~ trend + season)

##

## Residuals:

## Min 1Q Median 3Q Max

## -42.903 -7.599 -0.459 7.991 21.789

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 441.80044 3.73353 118.333 < 2e-16 ***

## trend -0.34027 0.06657 -5.111 2.73e-06 ***

## season2 -34.65973 3.96832 -8.734 9.10e-13 ***

## season3 -17.82164 4.02249 -4.430 3.45e-05 ***

## season4 72.79641 4.02305 18.095 < 2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 12.23 on 69 degrees of freedom

## Multiple R-squared: 0.9243, Adjusted R-squared: 0.9199

## F-statistic: 210.7 on 4 and 69 DF, p-value: < 2.2e-16#拟合完了

#画图

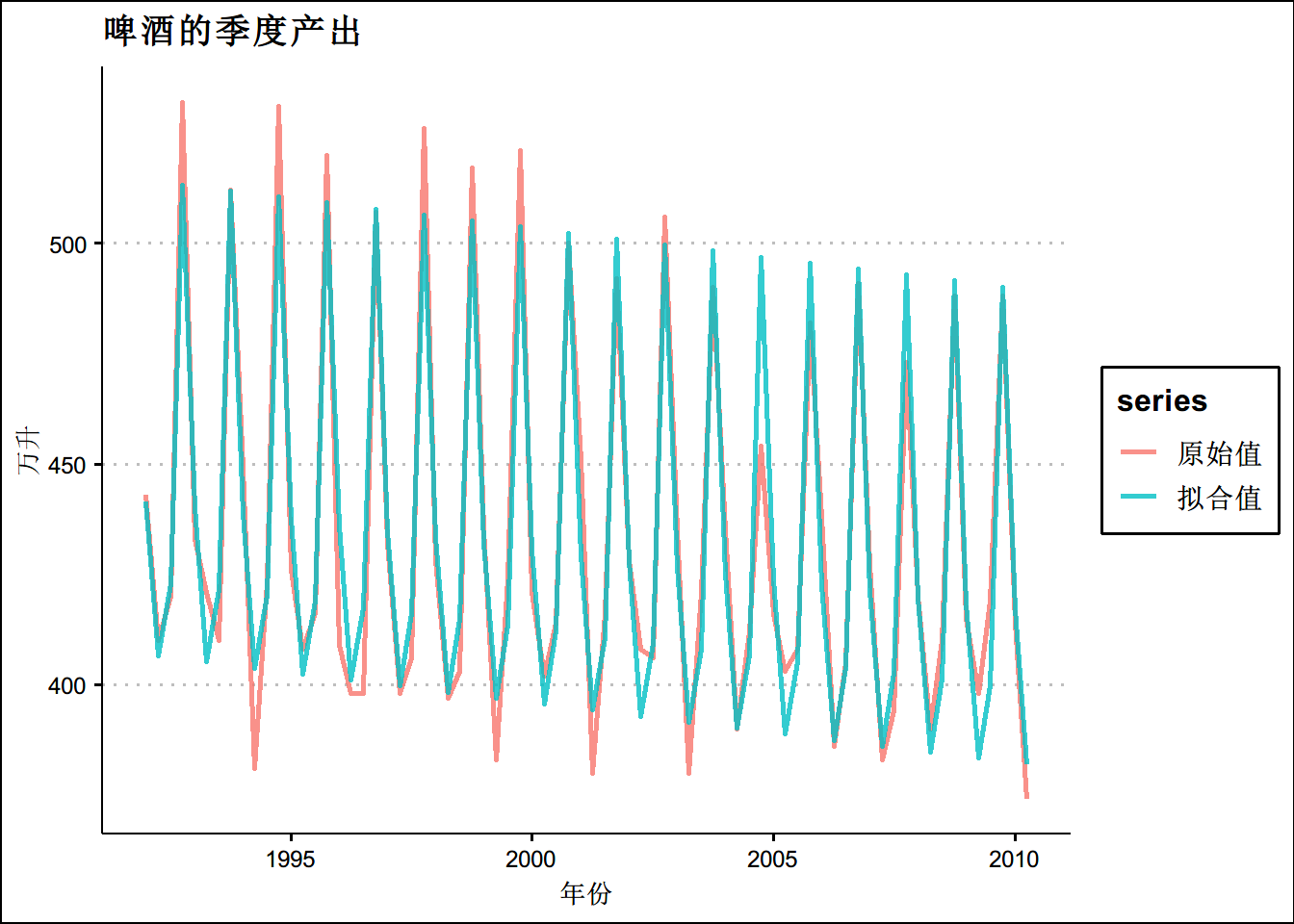

beer2_f <- ts.union(beer2,fitted(fit.beer))

colnames(beer2_f) <- c("原始值",'拟合值')

autoplot(beer2_f, series="真实值",size=1,alpha=0.8) +

xlab("年份") + ylab("万升") +

ggtitle("啤酒的季度产出")+

theme(text = element_text(family = "STHeiti"))+

theme(plot.title = element_text(hjust = 0.5)) +

theme_clean()

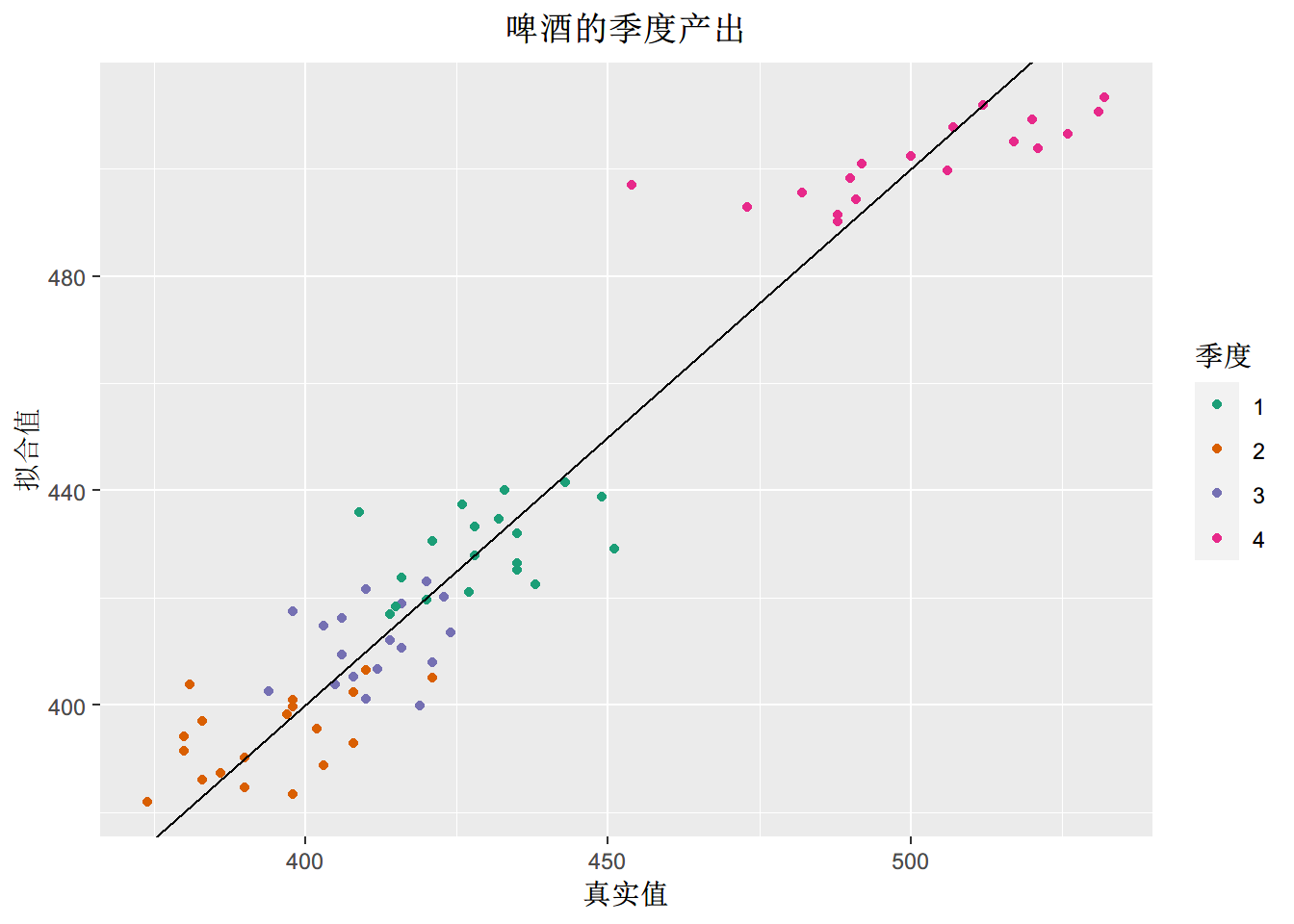

cbind(Data=beer2, Fitted=fitted(fit.beer)) %>%

as.data.frame() %>%

ggplot(aes(x=Data, y=Fitted, colour=as.factor(cycle(beer2)))) +

geom_point() +

ylab("拟合值") + xlab("真实值") +

ggtitle("啤酒的季度产出") +

scale_colour_brewer(palette="Dark2", name="季度") +

geom_abline(intercept=0, slope=1)+

theme(text = element_text(family = "STHeiti"))+

theme(plot.title = element_text(hjust = 0.5))

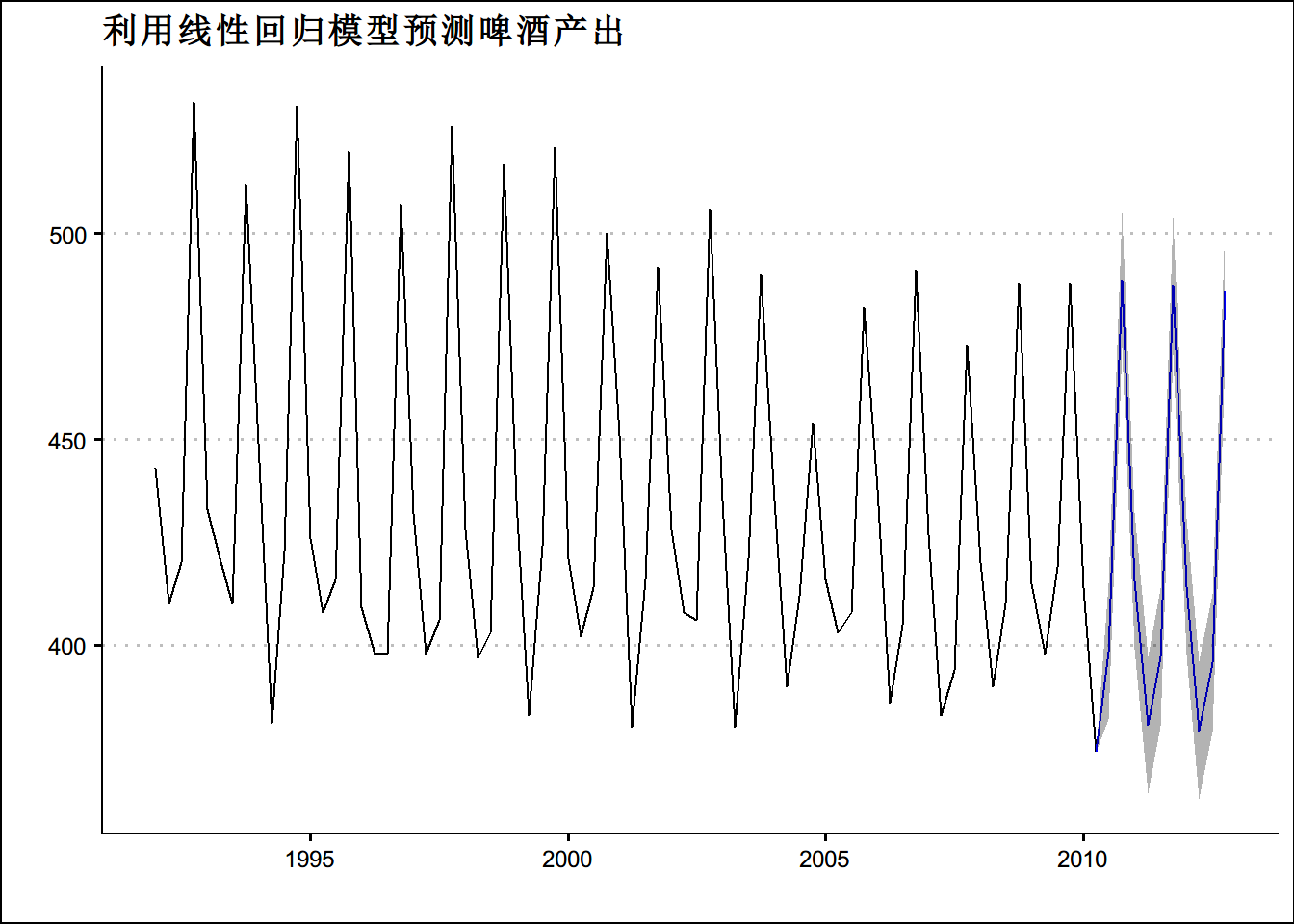

使用拟合好的模型进行预测

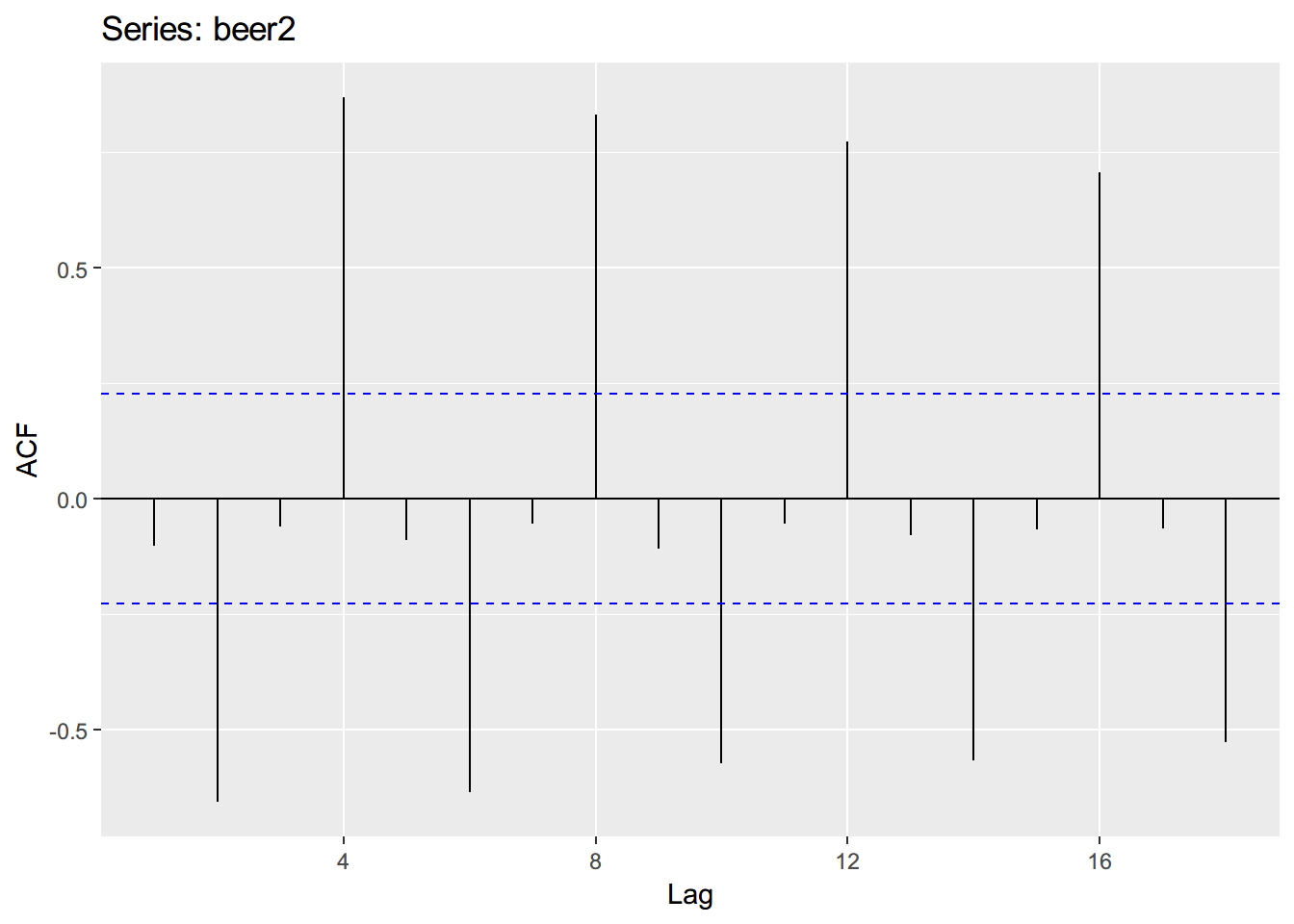

beer2 <- window(ausbeer, start=1992)

ggAcf(beer2)

fit.beer <- tslm(beer2 ~ trend + season)

fcast <- forecast(fit.beer)

summary(fcast)##

## Forecast method: Linear regression model

##

## Model Information:

##

## Call:

## tslm(formula = beer2 ~ trend + season)

##

## Coefficients:

## (Intercept) trend season2 season3 season4

## 441.8004 -0.3403 -34.6597 -17.8216 72.7964

##

##

## Error measures:

## ME RMSE MAE MPE MAPE MASE

## Training set -1.536051e-15 11.80909 9.029722 -0.06895219 2.08055 0.665348

## ACF1

## Training set -0.2499017

##

## Forecasts:

## Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

## 2010 Q3 398.4587 381.8746 415.0428 372.8900 424.0274

## 2010 Q4 488.7365 472.1524 505.3206 463.1678 514.3052

## 2011 Q1 415.5998 399.0029 432.1968 390.0113 441.1883

## 2011 Q2 380.5998 364.0029 397.1968 355.0113 406.1883

## 2011 Q3 397.0976 380.4421 413.7532 371.4188 422.7765

## 2011 Q4 487.3754 470.7199 504.0310 461.6966 513.0543

## 2012 Q1 414.2387 397.5669 430.9106 388.5347 439.9428

## 2012 Q2 379.2387 362.5669 395.9106 353.5347 404.9428

## 2012 Q3 395.7366 379.0028 412.4704 369.9371 421.5360

## 2012 Q4 486.0143 469.2806 502.7481 460.2149 511.8138autoplot(fcast) +

ggtitle("利用线性回归模型预测啤酒产出")+

theme(text = element_text(family = "STHeiti"))+

theme(plot.title = element_text(hjust = 0.5)) + theme_clean()

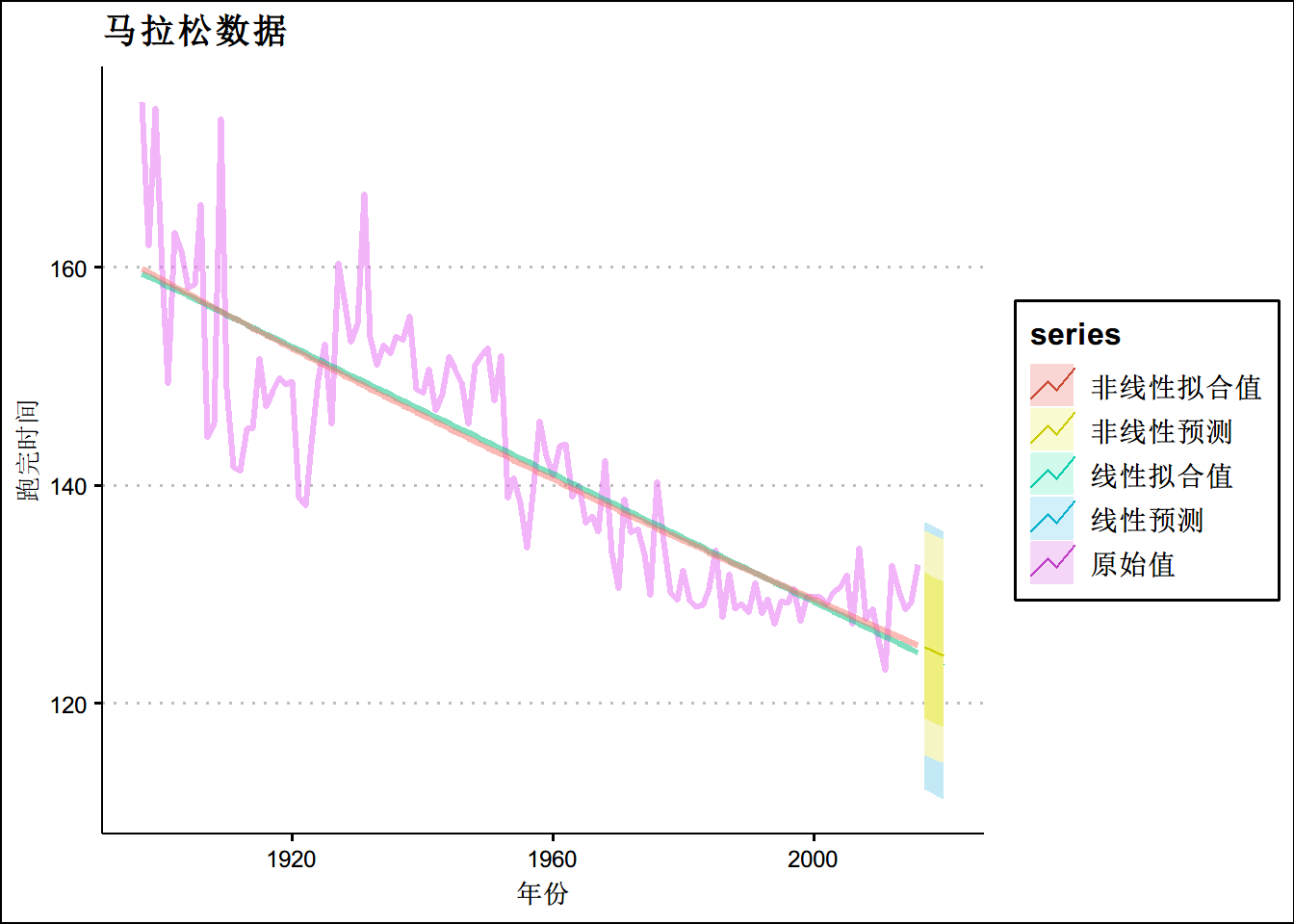

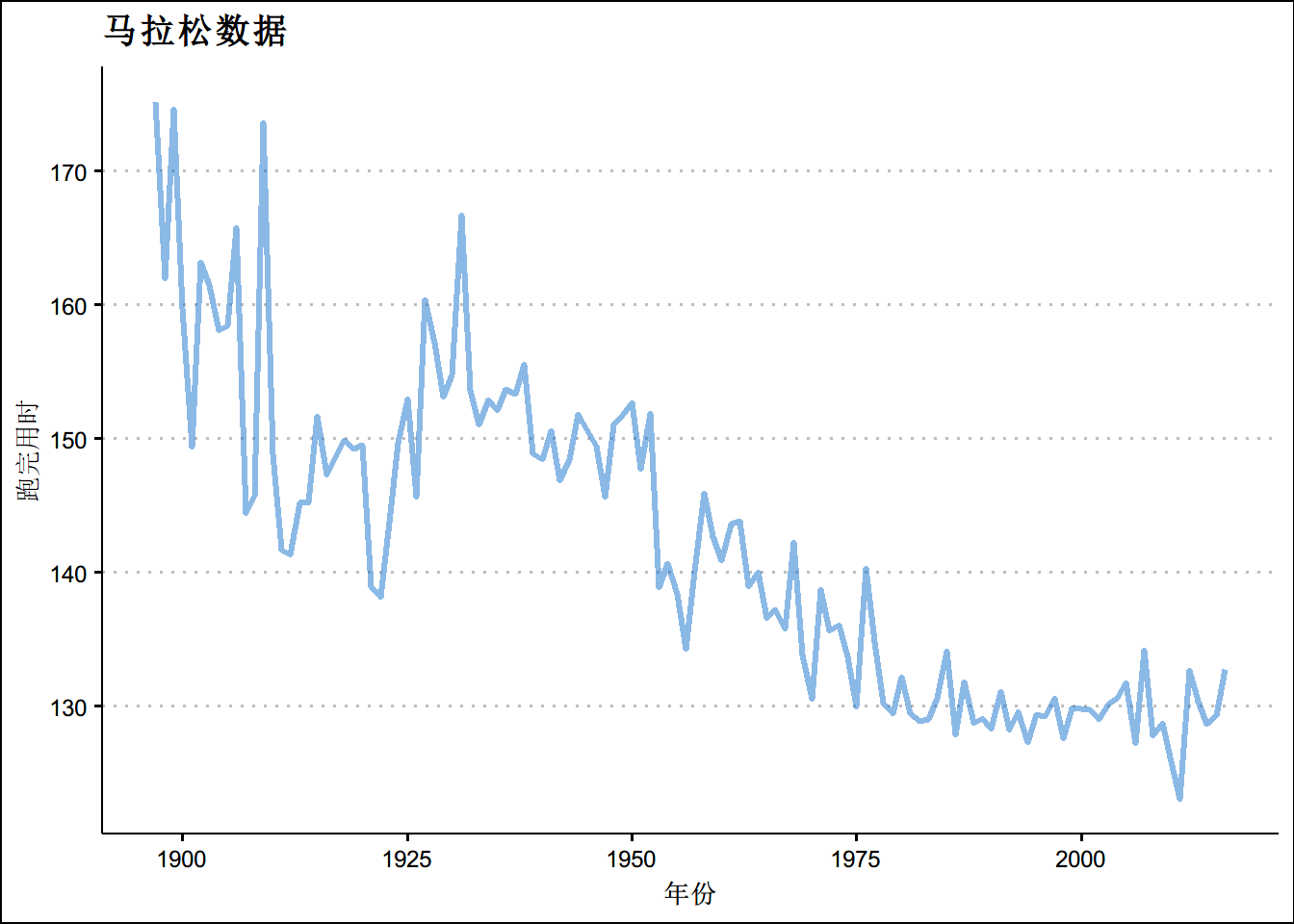

autoplot(marathon,size=1.1,alpha = 0.5,ts.colour = "dodgerblue3")+theme_clean()+

ggtitle("马拉松数据")+

xlab("年份")+

ylab("跑完用时")

#异方差现象library(forecast)

h <- 4 # 预测四期

fit.lin <- tslm(marathon ~ trend )

fcasts.lin <- forecast(fit.lin, h = h)

fit.exp <- tslm(marathon ~ trend , lambda = 0)

fcasts.exp <- forecast(fit.exp, h = h)

marathon_f <- ts.union(marathon,fitted(fit.lin),fitted(fit.exp))

colnames(marathon_f) <- c("原始值",'线性拟合值','非线性拟合值')

autoplot(marathon_f,size=1.1,alpha=0.5) +

ggtitle("利用线性回归模型预测啤酒产出")+

theme(text = element_text(family = "STHeiti"))+

theme(plot.title = element_text(hjust = 0.5)) + theme_clean()+

autolayer(fcasts.lin, series = '线性预测')+

autolayer(fcasts.exp,series = '非线性预测') +xlab('年份')+ylab('跑完时间')+

ggtitle("马拉松数据")